How Long Will $3 Million Last in Retirement?

- Megan Waters, CFP®

- Feb 13

- 18 min read

The answer depends on 5 factors many retirees overlook. We ran the numbers at 3 withdrawal rates — and the gap was 11 years.

Richard and Diane* built a $3 million portfolio over 35 years. Smart saving. Disciplined investing. And on the day Richard retired at 65, they felt confident. Three million should be more than enough.

Then their financial advisor ran the projections for a hypothetical portfolio earning a flat 5% average return . At $170,000 a year in withdrawals, their money runs out at age 88. At $130,000 a year, it lasts to 99. That's an 11-year difference — determined almost entirely by how much they pull out in the first few years.

The question isn't really whether $3 million is enough. It's whether you'll manage it in a way that makes it last.

Key Takeaways

$40,000/year in extra withdrawals costs 11 years of portfolio life — the difference between money lasting to age 89 vs. age 100.

The 4% rule ($120K) is a pre-tax number. After federal taxes, state taxes, and Medicare surcharges, your real spending power drops significantly.

Healthcare costs consume 14% of withdrawals at age 65 — and 46% by age 85, crowding out lifestyle spending even as your withdrawal rises with inflation.

Withdrawal sequencing alone can add 2.6–3.0 years of portfolio life.

State taxes can reduce portfolio values by $600,000 to $1 million when taking into account taxes and lost compounding.

The Roth conversion window between retirement and age 73 can potentially be the most valuable tax-planning opportunity most $3M retirees miss entirely.

What the 4% Rule Actually Means at $3 Million (And Why It's Misleading)

The 4% rule says you can withdraw 4% of your portfolio in year one, then adjust for inflation each year, and your money should last 30 years. At $3 million, that's $120,000 starting in year one.

But that number is pre-tax. It tells you almost nothing about what you can actually spend.

Let's trace what happens to that $120,000 in the real world. Say you're a married couple, both 65, pulling $120,000 from a traditional IRA. You also collect $40,000 in combined Social Security benefits.

First, the IRS taxes up to 85% of your Social Security once your combined income crosses $44,000 for couples. At $120,000 in IRA withdrawals, you blow past that threshold — so roughly $34,000 of your Social Security becomes taxable income too.

That gives you an Adjusted Gross Income (AGI) — basically, the income number the IRS uses to calculate your taxes — of about $154,000. After the standard deduction ($35,500 for a married couple both 65+, in 2026), your federal tax bill lands somewhere around $12,960.

Now here's where it gets worse. Medicare uses a number called MAGI — Modified Adjusted Gross Income — to set your premiums. It's essentially your AGI plus tax-exempt interest.

Cross $218,000 as a couple (2026), and you trigger IRMAA surcharges. IRMAA stands for Income-Related Monthly Adjustment Amount — it's a Medicare premium increase that kicks in at specific income levels.

At $154,000 in MAGI, you're safely below that line. But add a pension, rental income, or a Roth conversion on top of that $120,000 withdrawal — and you're suddenly in the danger zone. Cross the $218,000 threshold by even $1, and you pay an additional surcharge: roughly $2,300 per year for a couple at the first tier.

And here's the kicker: IRMAA uses cliff thresholds, not gradual increases. Go $1 over the line, and you pay the same penalty as someone who went $56,000 over.

Meanwhile, Morningstar's latest research puts the safe starting withdrawal rate at 3.9% for a 30-year horizon — not 4% - but close. On $3 million, that's the difference between $120,000 and $117,000 before you even factor in taxes.

The bottom line: Your real spending power from a $120,000 withdrawal is closer to $107,040 after federal taxes and $101,613 when you include a 5.75% state tax (assume Virginia).

In high-tax states like California or New York, it drops further. The 4% rule gives you a napkin number. It's not a retirement plan.

Learn more about why the 4% rule falls short for retirees with complex tax situations and what to use instead.

Three Scenarios: How Withdrawal Rates Change Everything

We ran three scenarios through our retirement projection calculator using identical assumptions except for the annual withdrawal amount. Here are the variables that remain the same across all three case studies.

Starting portfolio: $3,000,000

Retirement age: 65 (already retired, no additional contributions)

Portfolio return in retirement: 5% annually (after fees)

Inflation adjustment: 2.5% annually on withdrawals

Effective tax rate on withdrawals: 25%

Percent of portfolio withdrawal that is taxable: 100%

The only variable we changed in each case study was the initial annual withdrawal: $130,000, $150,000, and $170,000.

[Disclosure: The following projections are hypothetical illustrations based on the assumptions listed above. They do not represent the experience of actual clients. Hypothetical results have inherent limitations, including that they are prepared with the benefit of hindsight, assume a constant rate of return (which does not occur in real markets), and do not reflect actual trading or the performance of any specific client portfolio. Actual results will vary based on market performance, tax situation, fees, and individual circumstances.]

Scenario 1: $130,000/Year — The Conservative Path

Milestone | Age | Portfolio Value | Annual Withdrawal | After-Tax Income |

Year 1 | 65 | $3,000,000 | $130,000 | $97,500 |

Year 10 | 74 | $3,041,844.89 | $162,352.19 | $121,764.14 |

Year 20 | 84 | $2,633,011.53 | $207,824.52 | $155,868.39 |

Year 30 | 94 | $1,316,755.47 | $266,032.96 | $199,524.72 |

Year 34 | 98 | $382,245.79 | $293,650.61 | $220,237.96 |

Result: Portfolio lasts to age 99 — a full 35 years of retirement.

At a 4.3% initial withdrawal rate, the portfolio actually grows slightly in the first decade. That's because the 5% return outpaces the inflation-adjusted withdrawals early on.

But, after age 77 — the portfolio begins declining faster as inflation-adjusted withdrawals cross the $174,000 mark while the shrinking portfolio's return isn't enough to sustain the withdrawals.

The trade-off? Your after-tax income starts at $97,500. For a couple accustomed to a higher lifestyle, that might feel tight — especially in the first decade when they're most active.

Scenario 2: $150,000/Year — The Middle Ground

Milestone | Age | Portfolio Value | Annual Withdrawal | After-Tax Income |

Year 1 | 65 | $3,000,000 | $150,000 | $112,500 |

Year 10 | 74 | $2,793,823.38 | $187,329.45 | $140,497.08 |

Year 20 | 84 | $1,871,805.53 | $239,797.53 | $179,848.15 |

Year 25 | 89 | $964,599.77 | $271,308.89 | $203,481.67 |

Year 28 | 92 | $218,582.70 | $292,170.00 | $219,127.50 |

Result: Portfolio lasts to age 92 — 28 years of retirement.

This is the scenario many retirees may gravitate toward depending upon their lifestyle. A 5.0% initial withdrawal rate gives you $112,500 in after-tax income — roughly $15,000 more per year than the conservative path. But that extra spending costs you 7 years of portfolio life.

The critical inflection point comes around age 84. That's when the portfolio drops below $2 million and the math starts working against you. Inflation-adjusted withdrawals nearly reach $240,000, but the portfolio is generating only about $93,600 in returns. From there, depletion accelerates.

Scenario 3: $170,000/Year — The Aggressive Path

Milestone | Age | Portfolio Value | Annual Withdrawal | After-Tax Income |

Year 1 | 65 | $3,000,000 | $170,000 | $127,500 |

Year 10 | 74 | $2,545,801.88 | $212,306.70 | $159,230.03 |

Year 20 | 84 | $1,110,599.52 | $271,770.53 | $203,827.90 |

Year 24 | 88 | $105,387.15 | $299,983.82 | $224,987.86 |

Result: Portfolio lasts to age 88 — just 24 years of retirement.

At a 5.67% initial withdrawal rate, you get the highest starting income: $127,500 after taxes. But the portfolio never grows. It begins shrinking immediately and loses nearly half its value by age 82.

By age 84, you have just $1.11 million left — and your inflation-adjusted withdrawals are demanding over $270,000 per year.

If you retire at 65, this scenario means your money runs out before your 90th birthday. Given that a 65-year-old couple today has roughly a 50% chance that one spouse will live past 90, this is a coin flip on running out of money.

The Numbers That Matter

Same $3 million. Three different outcomes.

Scenario | Initial Withdrawal | Initial Withdrawal Rate | Portfolio Lasts To | Years of Retirement |

Conservative | $130,000/yr | 4.33% | Age 98 | 35 years |

Moderate | $150,000/yr | 5.0% | Age 92 | 28 years |

Aggressive | $170,000/yr | 5.67% | Age 88 | 24 years |

The cost of that extra $40,000/year in withdrawals? Eleven fewer years of retirement income.

These projections assume a steady 5% annual return. In reality, markets don't deliver steady returns — a 20% market drop in your first year of retirement does far more damage than the same drop in year 15. That's sequence of returns risk — and it can shave years off even the conservative scenario.

Why "Just Living Off Dividends" Doesn't Work at $3 Million

You might be wondering: Can I just live off the dividends?

This is one of the most popular strategies discussed on financial forums — and one of the most dangerous at the $3 million level.

Unfortunately, the math doesn't add up.

The S&P 500 Index dividend yield sits at roughly 1.15% as of February 13, 2026. The current yield to maturity on the S&P U.S. Aggregate Bond Index is 4.27% as of February 13, 2026. That means a standard 60/40 portfolio yields approximately 2.40%. On $3 million, that generates about $72,000 per year before taxes.

To reach $130,000 or more in dividend income, you'd need to concentrate in high-yield investments — introducing sector risk and potential for dividend cuts.

During the 2020 COVID crash, 306 U.S. companies cut or suspended dividends. And here's the tax problem: dividends are taxable whether you reinvest them or not.

Qualified dividends at high income levels face 15% plus the 3.8% NIIT — an effective 18.8% rate. You lose the ability to choose when to realize income, which is critical for managing IRMAA thresholds and tax brackets.

A total-return approach — dividends plus systematic share sales — gives you better tax control, better diversification, and historically better outcomes.

The flexibility to choose when and how much income to realize is one of the most valuable planning tools available to $3 million retirees.

The Factor That Can Add Years to Your Portfolio: Withdrawal Sequencing

The three scenarios above assume you're pulling from a single pool of money. In reality, most $3 million retirees have money spread across three types of accounts: taxable brokerage accounts, traditional IRAs or 401(k)s, and Roth IRAs. The order you draw from these accounts matters enormously.

The conventional wisdom — draw from taxable accounts first, then traditional, then Roth last — sounds logical. Let tax-deferred accounts compound longer. Preserve the Roth for last.

It's actually suboptimal for most $3 million portfolios. As financial planner Michael Kitces has shown, this approach can be too good at deferral. Your traditional IRA grows so large that Required Minimum Distributions (RMDs) — the annual withdrawals the IRS forces you to take starting at age 73 — push you into much higher tax brackets than necessary.

Research from William Reichenstein at the TIAA Institute found that optimized withdrawal sequencing added 2.6 years of portfolio life for a $2 million portfolio — and even more for larger ones. Separate research published in the Financial Analysts Journal found that tax-efficient strategies could extend portfolio longevity by more than three years in many cases. That's meaningful extra runway — achieved through smarter tax planning, not higher-risk investments. The trade-off: it requires careful coordination across accounts and tax brackets each year, and getting the sequencing wrong can trigger unexpected tax bills.

The strategies that outperform the conventional approach include Roth conversions during the low-income years between retirement and age 73, tax bracket filling across multiple account types, and capital gains harvesting at the 0% rate while taxable income remains below $98,900 for married couples filing jointly (2026, per IRS Revenue Procedure 2025-32).

A January 2026 Journal of Accountancy study found that a laddered Roth conversion strategy produced $124,144 in lifetime tax savings and a $655,791 difference in portfolio value by age 100 — boosting portfolio returns by 0.6% over the life of the plan.

The Myth: "I Should Go Ultra-Conservative to Protect What I've Built"

Many $3 million retirees shift entirely into bonds, CDs, and money market funds the moment they retire. It feels safe. It's actually one of the most dangerous moves you can make.

Here's why: the 4% rule itself was built on a portfolio with 50% stocks. An all-bond portfolio actually has lower survival rates over 30 years than a balanced portfolio.

At 3% inflation, a $3 million all-bond portfolio yielding 4–5% barely keeps pace in real terms. After taxes on bond interest — which is taxed at ordinary income rates up to 37% plus 3.8% NIIT, totaling 40.8% for high-income earners — real returns may be negative.

The opportunity cost is massive. If a balanced allocation earns 7% versus 4% from bonds over 25 years, the compounding difference on $3 million reaches into the millions of dollars in foregone growth.

And bond interest generates fully taxable income at the highest rates, while long-term capital gains on equities qualify for the lower 15–20% rate.

Research shows that dynamic withdrawal strategies allow starting rates of 5.0% or higher with moderate flexibility — but these require equity allocation to function.

The better approach could be to maintain 40–60% in equities even in retirement, with 3–5 years of spending in cash and bonds as a buffer. Think of it as a bucket strategy — roughly $240,000 in cash for near-term needs, $480,000 in bonds for medium-term stability, and $2.28 million in diversified equities as the growth engine.

This lets you weather 5 or more years of market downturns without forced selling while keeping the growth you need to outpace inflation and healthcare costs.

The trade-off is real: you'll see more portfolio volatility month-to-month. But the data consistently shows that accepting short-term fluctuation extends long-term portfolio life.

How Healthcare Costs Silently Eat Your $3 Million

Healthcare is the expense most retirement calculators underestimate — and the one that escalates fastest.

Fidelity's 2025 Retiree Health Care Cost Estimate projects that a 65-year-old couple needs $345,000 in after-tax savings for healthcare throughout retirement. That's 11.5% of a $3 million portfolio dedicated to a single expense category — and it excludes long-term care, dental, and vision.

The picture gets worse with more comprehensive estimates. The HealthView Services 2026 Retirement Healthcare Costs Data Report projects total lifetime healthcare costs for a healthy 65-year-old couple — including Parts B, D, Medigap Plan G, dental premiums, and all out-of-pocket expenses — at $661,812 in today's dollars, or $955,411 in future value.

Here's what makes healthcare uniquely dangerous for portfolio longevity: it inflates far faster than everything else. HealthView Services projects long-term retirement healthcare inflation at 5.8% — more than double the projected 2.4% growth in Social Security cost-of-living adjustments. Medicare Part B premiums alone jumped 9.7% from 2025 to 2026 ($185 to $202.90 per month), according to CMS.

What this means for your $3 million portfolio at a 4% withdrawal ($120,000/year), based on HealthView Services' projections for a couple with traditional Medicare, Medigap Plan G, and dental coverage:

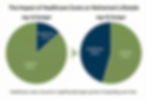

Your Age | Annual Healthcare Cost (Couple) | % of Your Withdrawal |

65 (Year 1) | ~$17,000 | 14.2% |

75 | ~$30,000 | 25.0% |

85 | ~$55,500 | 46.3% |

By age 85, healthcare consumes roughly half of a 4% withdrawal — crowding out lifestyle spending dramatically.

Your "lifestyle withdrawal rate" — the money actually available for housing, travel, food, and enjoyment — drops from 4.0% to roughly 3.4% in the first year and declines further every year after.

And then there's long-term care. Seven out of ten people reaching age 65 will need some form of long-term care, according to the U.S. Department of Health and Human Services. A private-room nursing home costs $127,750 per year (Genworth/CareScout 2024 Cost of Care Survey). A three-year stay costs approximately $383,250 — consuming 12.8% of the entire $3 million portfolio in a single event.

Read more about planning for healthcare costs in retirement and why it requires a dedicated strategy.

Where You Live Can Cost You $600K–$1 Million in Retirement

State taxes are one of the most underestimated drags on portfolio longevity. Every dollar withdrawn for state taxes is a dollar that can't compound — and at a 6% return, $10,000 withdrawn today represents approximately $57,000 in lost value over 30 years.

Here's what a single filer withdrawing $150,000 annually faces in different states (2025 tax year, with standard deductions applied):

State | Annual State Tax | 30-Year Total Impact (Tax + Lost Compounding) |

FL, TX, NV, PA, IL | $0 | $0 |

Virginia | ~$7,860 | ~$620K |

California | ~$9,960 | ~$790K |

NY + NYC | ~$13,330 | ~$1.05M |

Virginia's tax is calculated using the state's four-bracket structure (2%–5.75%) with the 2025 standard deduction of $8,750. California's figure reflects the state's nine-bracket system (1%–12.3%) with the 2025 standard deduction of $5,706. The New York figure combines state income tax (4%–6% at this income level) plus New York City tax (3.078%–3.876%), with the $8,000 standard deduction.

Important note on New York: Retirees age 59½ and older can exclude up to $20,000 of qualified retirement account income (IRA, 401(k), private pension) from New York State and NYC taxable income. If your $150,000 comes entirely from retirement accounts, the NY + NYC tax drops to approximately $11,900 — and the 30-year impact falls to roughly $940K. The figures above assume a mix of income sources where the full $20,000 exclusion may not apply.

Pennsylvania is the stealth winner for retirees. While it has a 3.07% flat income tax, PA fully exempts IRA distributions after age 59½, 401(k) distributions after retirement, pension income, and Social Security — making it functionally equivalent to Florida or Texas for retirement income. Illinois offers similar full exemptions on all retirement income, including Social Security, pensions, IRA distributions, and 401(k) withdrawals, despite its 4.95% flat income tax on other income. Mississippi also fully exempts all retirement income from state taxation.

Put it in monthly terms: a New York City retiree withdrawing $150,000 takes home roughly $136,700 after state and city taxes.

A Florida retiree keeps the full $150,000 for federal taxes and spending. That's over $1,100 per month less for housing, healthcare, and life — every single year for 30 years.

State taxes don't make or break a retirement on their own. But combined with federal taxes, healthcare inflation, and the compounding effect of every dollar withdrawn early, they're part of an erosion that turns a comfortable $3 million into a tight $3 million faster than most people expect.

How Long Will $3 Million Last? Check These Numbers

Before you talk to any advisor, check these numbers yourself. You can find most of them on your tax return and account statements. If you are a client, we do this for you.

1. Your actual withdrawal rate. Take your total annual withdrawals from all retirement accounts and divide by your current portfolio value. If it's above 5%, you're on the aggressive path. Above 5.5%, and you're in the danger zone for a 30-year retirement.

2. Your Modified Adjusted Gross Income (MAGI). Find this on line 11 of your most recent Form 1040. If you're a couple and this number is approaching $218,000, you're near the first IRMAA cliff. Every dollar over that threshold costs you $2,297 per year in Medicare surcharges.

3. Your account mix. What percentage of your $3 million is in traditional (tax-deferred) accounts versus Roth (tax-free) versus taxable brokerage? If more than 70% sits in traditional IRAs or 401(k)s, you may be setting up a massive RMD problem at age 73. You could also have a massive RMD problem if your IRA balances are over $1 million.

4. Your state tax rate on retirement income. Look up whether your state exempts retirement income (PA, IL, MS, IA do). If you're in a high-tax state, calculate what you're paying annually — and what that costs over 30 years of compounding.

5. Your healthcare cost assumption. Are you budgeting $345,000 or more for a couple's lifetime healthcare costs? If your retirement plan doesn't explicitly model healthcare inflation at 5%+ annually, it's underestimating one of your largest expenses.

If even two of these numbers surprise you, it's worth a deeper conversation about your withdrawal strategy.

The Covenant Wealth Advisors Approach

The three scenarios above assume a steady 5% return and a fixed tax rate. Real life is messier — and that's where integrated planning creates the most value.

At Covenant Wealth Advisors, we don't just pick a withdrawal rate and hope. We model the interactions between withdrawal sequencing, tax bracket management, IRMAA threshold planning, Roth conversion timing, healthcare cost projections, and state tax implications — because these factors compound against each other in ways that simple calculators can't capture.

If you are interested in working with us, you may request a free strategy session here.

Academic research suggests that this kind of integrated, tax-aware approach can extend portfolio life by 2.6–3.0 years.

On a $3 million portfolio over 30 years, that compounding advantage can translate into hundreds of thousands of dollars in preserved wealth. Results vary significantly based on individual tax situations, account types, market conditions, and other factors — not every retiree will see the same benefit.

That's the difference between running out of money in your 80s and having a portfolio that supports you — and potentially your heirs — well into your 90s.

The catch: this level of planning requires ongoing monitoring and adjustment. Tax laws change. Markets fluctuate. Healthcare costs rise. A plan built once and left alone will underperform a plan that adapts. That's the trade-off — and it's one that's worth making.

Want Our Team to Just Do Your Retirement Planning for You? Schedule Your Strategy Session!

Investment Management — built around your retirement income needs, not a generic model

Tax Planning For Retirement — Roth conversions, withdrawal sequencing, IRMAA strategies

Retirement Income Planning — a clear plan so you know your money won't run out

Award Winning* | Fee-Only Fiduciary | Serving Clients Nationwide

Frequently Asked Questions

How Long Will $3 Million Last in Retirement at a 4% Withdrawal Rate?

At a 4% withdrawal rate ($120,000/year), $3 million lasts approximately 30 years before taxes and inflation adjustments — the original timeframe the 4% rule was designed for.

However, after accounting for federal taxes (roughly $18,000–$22,000 depending on filing status and Social Security income), potential IRMAA Medicare surcharges ($2,300+/year for couples above $218,000 MAGI in 2026), and inflation-adjusted withdrawals that grow each year, the effective portfolio life may be shorter.

Our projections using a 5% return and 2.5% inflation show a $130,000 initial withdrawal (4.3% rate) lasting to approximately age 99. But, that's a simple straight line method and we also reccommend more rigourous testing via Monte-Carlo stress testing.

Is $3 Million Enough to Retire at 65?

For many retirees, yes — but it requires active management, not a set-it-and-forget-it approach. At $3 million, your withdrawal rate, tax strategy, account mix, state of residence, and healthcare planning all significantly impact how long the money lasts.

A 65-year-old couple today has roughly a 50% chance that one spouse will live past 90, meaning you may need 25–35 years of retirement income.

The difference between an unmanaged and an optimized $3 million portfolio can be measured in years of additional retirement security and hundreds of thousands in preserved wealth.

What is a Safe Withdrawal Rate for a $3 Million Portfolio?

Morningstar's December 2025 research puts the safe starting withdrawal rate at 3.9% for a 30-year retirement with 90% confidence. On $3 million, that's $117,000/year before taxes. However, "safe" depends heavily on your specific situation.

Dynamic withdrawal strategies that adjust spending based on portfolio performance — like the "guardrails" approach Morningstar tested — allow starting rates of 5.2% or higher with moderate flexibility. But they require maintaining equity allocation and accepting some variability in annual income. Learn more about safe withdrawal rates in retirement.

How Does Sequence of Returns Risk Affect a $3 Million Portfolio?

Sequence of returns risk means the order your investment returns come in matters more than the long-term average. A 20% market drop in Year 1 of retirement does far more damage than the same drop in Year 15 — because you're selling shares at depressed prices to fund withdrawals, permanently reducing the portfolio's recovery potential.

WealthTrace modeling shows that a retirement portfolio with a base-case 85% success probability can drop to just 36% success when a 2001-style bear market hits within the first two years. The good news? Diversifying across multiple asset classes — growth stocks, value stocks, international developed, emerging markets, and bonds — brought the bear market scenario back up to 77% success.

This is why building resilience against sequence of returns risk is critical — whether through diversification, maintaining a cash buffer covering several years of spending, or both.

Should I Do Roth Conversions with a $3 Million Portfolio?

For most $3 million retirees with the majority of assets in traditional IRAs, Roth conversions during the years between retirement and age 73 (when RMDs begin under SECURE 2.0) represent one of the most valuable tax-planning opportunities available.

You're converting at potentially lower tax rates — filling the 10%, 12%, and 22% brackets (now permanent under OBBBA) — to avoid future RMDs that could push you into the 24–32% brackets and trigger IRMAA surcharges.

A January 2026 Journal of Accountancy study found that laddered Roth conversions produced $124,144 in lifetime tax savings and a $655,791 difference in portfolio value by age 100.

The trade-off: you pay the tax bill now, and if you need that cash within five years, it can reduce your financial flexibility. Learn more about how Roth conversions work.

How Do State Taxes Affect How Long $3 Million Lasts?

Significantly. A single filer withdrawing $150,000/year in New York City pays approximately $13,300 in state and city taxes annually — totaling roughly $1.05 million in cumulative portfolio impact over 30 years when you factor in lost compounding at a 6% return. (Note: New York retirees age 59½+ can exclude up to $20,000 of qualified retirement income, which could reduce this figure further.)

That's the equivalent of $600,000–$1 million in lost wealth compared to a retiree in a zero-income-tax state like Florida, Texas, or Nevada.

Pennsylvania and Illinois are hidden gems — both fully exempt retirement income from state taxation, making them functionally equivalent to no-income-tax states for retirees.

Ready to get your retirement portfolio on track?

Contact us today for a Free Strategy Session.

About the author:

Financial Advisor

Megan Waters is a CERTIFIED FINANCIAL PLANNER™ professional and Financial Advisor at Covenant Wealth Advisors. Megan has over 14 years of experience in the financial services industry.

Raised in Williamsburg, VA, Megan graduated from the Honors College at the College of Charleston with a BS in Economics and a minor in Environmental Studies.

Disclosures: *The scenario regarding "Richard and Diane" is a hypothetical illustration used to demonstrate planning concepts. It does not represent the experience of actual clients. Hypothetical results have inherent limitations, including that they are prepared with the benefit of hindsight and do not reflect actual trading or the performance of any specific client portfolio. Covenant Wealth Advisors is a registered investment advisor with offices in Richmond, Reston, and Williamsburg, VA. Registration of an investment advisor does not imply a certain level of skill or training. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. The views and opinions expressed in this content are as of the date of the posting, are subject to change based on market and other conditions. This content contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. This article was written and edited by a CERTIFIED FINANCIAL PLANNER™ professional with the assistance of AI. No advice may be rendered by Covenant Wealth Advisors unless a client service agreement is in place. Hypothetical examples are fictitious and are only used to illustrate a specific point of view. Diversification does not guarantee against risk of loss. While this guide attempts to be as comprehensive as possible, no article can cover all aspects of retirement planning. Be sure to consult an advisor for comprehensive advice.