What Is the Gift Tax Rate? Federal Limits and How to Avoid It

- Andrew Casteel CFP®

- May 22

- 13 min read

Updated: May 30

David and Sarah Hartman wanted to help their daughter buy her first home. They had $4 million saved and figured a $1 million gift of Apple stock would be cleaner than a check.

Disclosure: The scenario regarding "David and Sarah Hartman’" is a hypothetical illustration used to demonstrate planning concepts. It does not represent the experience of actual clients. Hypothetical financial planning illustrations have inherent limitations, including that they are prepared with the benefit of hindsight and do not reflect actual results of any specific client situation.

They had owned the stock for 22 years. Cost basis: $200,000. Fair market value: $1,000,000. Their CPA confirmed they would owe no gift tax. True. They filed Form 709, used a slice of their $30,000,000 (2026) lifetime exemption, and felt smart.

What no one mentioned: under IRC §1015, their daughter inherited their basis. When she sold, she owed long-term capital gains tax on the full $800,000 of appreciation. The combined rate was 23.8% — the 20% long-term capital gains rate plus the 3.8% Net Investment Income Tax that kicks in above $250,000 MFJ.

The total tax was about $190,400. A hold-to-death plan would have eliminated it under IRC §1014, which steps the basis up to fair market value at death.

In our planning work with HNW families across the country, we see this trade-off come up often.

Key Takeaways

The federal gift tax rate graduated from 18% to 40% under IRC §2001(c), applied to cumulative lifetime taxable gifts above the lifetime exemption. The top 40% rate begins above $1,000,000 of cumulative taxable transfers.

The 2026 annual gift exclusion is $19,000 per recipient, per donor ($38,000 with gift-splitting). No filing required at or below.

The 2026 lifetime exemption is $15,000,000 per individual / $30,000,000 per couple, made permanent by the One Big Beautiful Bill Act (OBBBA, PL 119-21).

The donor pays gift tax — never the recipient. The recipient owes nothing on their federal income tax return.

Direct payments to schools and medical providers are unlimited and tax-free under IRC §2503(e) — but only when paid directly, not reimbursed.

Lifetime gifts of low-basis assets often (but, not always) cost more than they save. A $1,000,000 gift of low-basis stock can create about $190,400 of capital-gains tax that a §1014 stepped-up bequest would eliminate.

What Is the Federal Gift Tax Rate in 2026?

The federal gift tax rate graduated from 18% to 40% under IRC §2001(c). It applies only to cumulative lifetime taxable gifts above the $15,000,000 (2026) lifetime exemption. The first $19,000 per recipient each year is excluded entirely. Many donors never owe a dollar of gift tax.

The rate schedule appears in the IRS Instructions for Form 709 as the Table for Computing Gift Tax.

Taxable Gift Range | Marginal Rate |

First $10,000 | 18% |

$10,001 - $20,000 | 20% |

$20,001 - $40,000 | 22% |

$40,001 - $60,000 | 24% |

$60,001 - $80,000 | 26% |

$80,001 - $100,000 | 28% |

$100,001 - $150,000 | 30% |

$150,001 - $250,000 | 32% |

$250,001 - $500,000 | 34% |

$500,001 - $750,000 | 37% |

$750,001 - $1,000,000 | 39% |

Over $1,000,000 | 40% |

Source: IRS Instructions for Form 709, Table for Computing Gift Tax (IRC §2001(c)).

The reason almost no one pays: Form 709 computes a tentative tax on cumulative lifetime taxable gifts using the §2001(c) schedule.

It then offsets that with the unified credit — the credit equivalent of the $15,000,000 (2026) basic exclusion. Tax is owed only when cumulative taxable gifts exceed $15,000,000 (26 U.S. Code § 2010).

Gift tax is its own transfer tax. It is not paired with income or capital-gains brackets.

How Much Can You Gift Tax-Free in 2026?

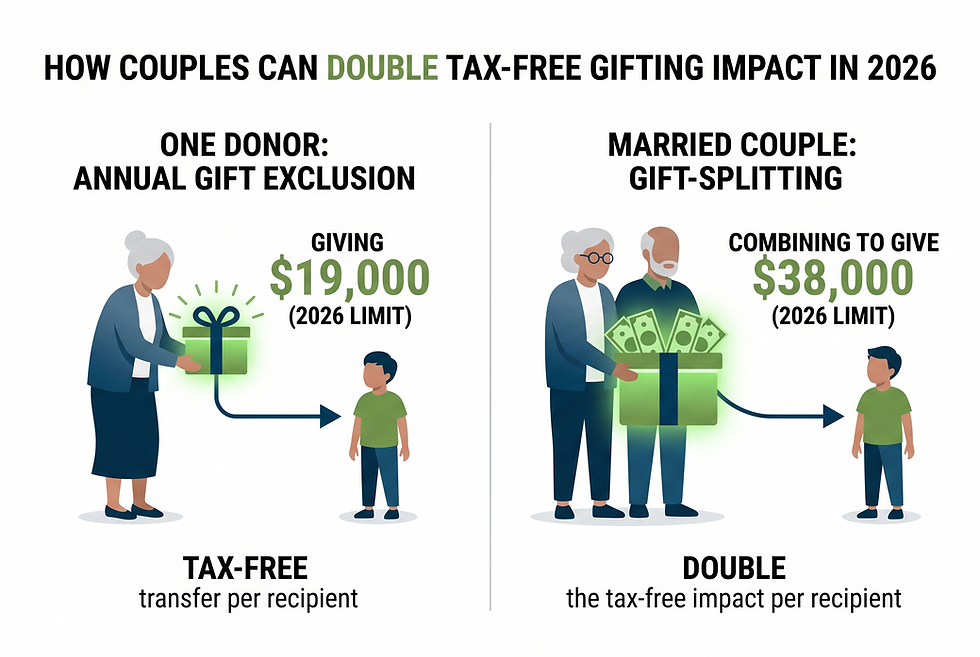

A single donor can give up to $19,000 (2026) per recipient with no filing or tax. A married couple electing gift-splitting can give $38,000 (2026) per recipient.

There is no limit on the number of recipients — a grandparent can give $19,000 to each of ten grandchildren ($190,000 total) without touching lifetime exemption.

The annual exclusion under IRC §2503(b) is per donor, per recipient, per year. It does not roll over.

Gift-splitting under IRC §2513 lets a married couple treat all third-party gifts during the year as half from each spouse. The effect doubles the exclusion to $38,000 per recipient, even when only one spouse owns the asset. The election is made via a separate Notice of Consent on Form 709 (updated IRS rules).

Two 2026 figures many articles miss. First, the non-citizen spouse annual exclusion is $194,000 (2026) under IRC §2523(i) — gifts between U.S.-citizen spouses are unlimited.

Second, the generation-skipping transfer (GST) tax exemption is $15,000,000 (2026) with a flat 40% rate on transfers above it (Miller Canfield). GST covers gifts that "skip" a generation — typically grandparent to grandchild.

What Is the Lifetime Gift Tax Exemption?

The 2026 lifetime gift and estate tax exemption is $15,000,000 per individual / $30,000,000 per couple.

It was made permanent by the One Big Beautiful Bill Act (PL 119-21, §70106), signed July 4, 2025, with annual inflation adjustments. The pre-2026 sunset that drove the "gift before it disappears" urgency is gone under current law.

The exemption is unified — one pool covers gifts during life and bequests at death. Every dollar of taxable lifetime gifting reduces the exemption available at death (26 U.S. Code § 2010).

OBBBA permanence shifted the strategic question. The old framing was urgency. The new framing is which lever, in which order, and with which assets.

The exemption is also portable between spouses through the DSUE (Deceased Spouse's Unused Exclusion). A surviving spouse inherits the first-to-die's unused exemption only if Form 706 is filed within 5 years of the first death (Mercer Advisors).

DSUE is not automatic. And "permanent" means until Congress changes it.

Who Pays the Gift Tax — the Giver or the Recipient?

The donor pays the gift tax — never the recipient. Under IRC §2502(c), legal liability sits with the giver. The recipient owes nothing on their federal income tax return and has no filing duty.

You can hand your daughter $50,000 and she files nothing. She owes nothing. She does not even mention it.

Does the Recipient Report the Gift?

No. Under federal law, gifts received are not taxable income to the recipient. The donor — not the recipient — files Form 709 and tracks lifetime exemption usage.

The only real exception is a "net gift" arrangement where the recipient agrees to pay the tax by contract. That setup is rare and must be documented.

One footnote: if the gift produces income after it lands — interest, dividends, rents — the recipient pays income tax on that income going forward. The gift is tax-free. The future yield is not.

Filing Form 709: When Does a Gift Trigger Paperwork?

A donor must file Form 709 when any single recipient gets more than $19,000 (2026) from one donor in a calendar year. This holds even if no tax is due.

The form is also required for gift-splitting elections, gifts of future interests, generation-skipping transfers, and 529 superfunding. The deadline is April 15 of the year after the gift.

Filing does not mean owing tax. Many 709 filings just report the gift, apply the unified credit, and reduce remaining lifetime exemption.

Two points HNW donors should know.

The 3-year statute of limitations under IRC §6501 only starts running when Form 709 is filed and fully discloses the gift. A gift never reported has no SOL. The IRS can revalue it decades later, often during estate audits.

This is general framing only. The §6501(c)(9) rules are complex. Talk with a tax attorney or CPA about your case. This matters most with gifts of complex assets like closely-held stock, partnership stakes, real estate, or art.

Late-filing penalties are 5% per month of unpaid tax (up to 25%), plus 0.5% per month for late payment (IRS). Many filings owe no tax, so the dollar penalty is often $0 — but the missed SOL clock is the real cost.

When Does Gifting Backfire? The Basis Step-Up Trade-Off

A lifetime gift carries the donor's cost basis under IRC §1015. A bequest at death gets a basis step-up to fair market value under IRC §1014.

For HNW couples whose total estate sits under the $30,000,000 (2026) couple exemption, this matters. Gifting low-basis assets during life often creates capital-gains tax a hold-to-death plan would have wiped out.

This is a very expensive oversight when it comes to gift tax rates. Here is the math.

In the Generic Advice version of their story, the Hartmans' capable CPA gives clean advice. The CPA says they can give Sarah $1,000,000 of Apple stock without owing gift tax, since they have $30,000,000 of exemption. Correct on gift tax. Basis is not part of that conversation.

Sarah inherits the $200,000 basis. When she sells:

Sale proceeds: $1,000,000

Carryover basis: $200,000

Long-term capital gain: $800,000

Federal LTCG at 20%: $160,000

Net Investment Income Tax at 3.8%: $30,400

Total federal capital-gains tax: $190,400

Hold the same shares to death under §1014, and Sarah's basis steps up to fair market value. A sale the next day produces about $0 of gain.

IRC §1014(e) blocks the step-up in one narrow case. The asset must be gifted to a donor who dies within one year. And the asset must then pass back to the original donor.

That guardrail aside, the rule is clean: low-basis assets are for bequeathing, not gifting.

The High-Net-Worth Reality

If your total estate is under $30,000,000 (2026), gift cash. Gift IRA distributions you would otherwise spend. Gift via 529. Gift via direct tuition. And hold your low-basis stock until the §1014 step-up does the work. The gift tax rate is not the constraint. The basis trade-off is.

How to Avoid Gift Tax: A 5-Strategy Framework

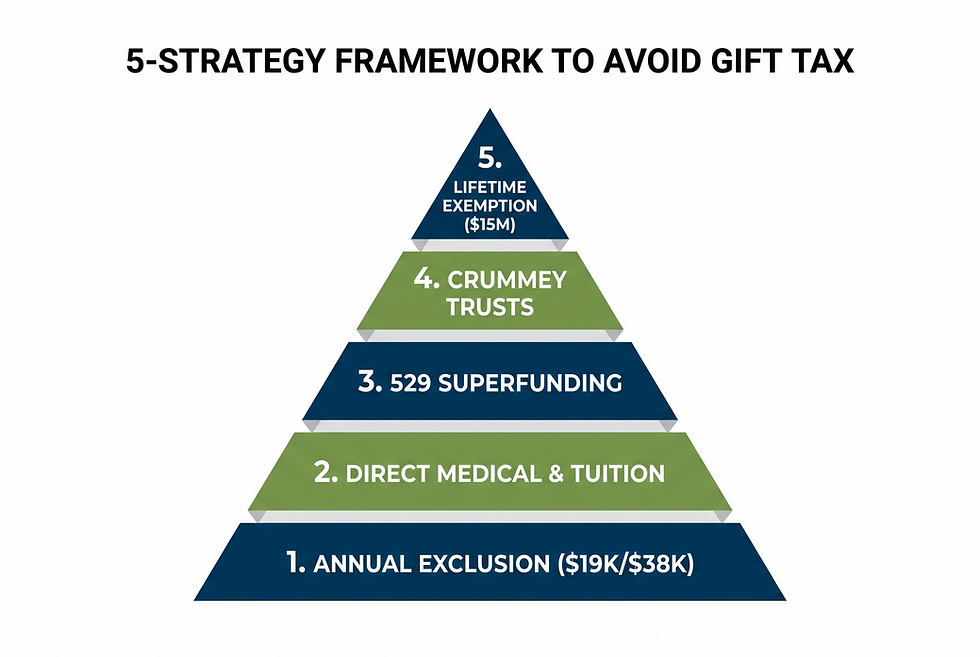

Many HNW couples never owe gift tax. Five tools, used together, cover almost every family transfer they will ever want to make.

The strategies stack: annual exclusion plus gift-splitting, direct medical and tuition payments, 529 superfunding, Crummey trusts, and the lifetime exemption itself.

1. Stack the annual exclusion with gift-splitting

Each spouse can give $19,000 (2026) to each child, grandchild, niece, or nephew. Gift-splitting doubles that to $38,000 per recipient.

A couple with three children and six grandchildren can move $342,000 a year ($38,000 × 9) out of the taxable estate without touching lifetime exemption.

2. Pay schools and medical providers directly under §2503(e)

IRC §2503(e) fully excludes qualified transfers from gift tax. No annual or lifetime cap. A grandparent can pay $200,000 of a grandchild's tuition with no tax fallout — as long as the check goes straight to the school.

The trap: paying the grandchild who then pays the school breaks the rule. Tuition only — not room, board, fees, or books. Medical costs must qualify as §213(d) expenses, paid straight to the provider or insurer (ArentFox Schiff).

3. Superfund a 529 for 5 years up front

Under IRC §529(c)(2)(B), a donor can choose to treat a single 529 gift as if spread over 5 years. In 2026, that allows up to $95,000 per beneficiary by a single donor or $190,000 per beneficiary by a married couple electing gift-splitting.

Funds grow tax-free, with no lifetime exemption used. No further gifts to that beneficiary for 5 years. If the donor dies before year 5, the unused portion pulls back into the gross estate. Form 709 is required even when no tax is due (Fidelity).

4. Use a Crummey trust for present-interest treatment

Gifts to a trust are treated as future-interest gifts by default. They do not qualify for the $19,000 (2026) annual exclusion.

A Crummey trust (The Tax Adviser) gives each beneficiary a short withdrawal right (30-60 days) over each contribution. That converts the gift into a present interest — a current legal right to enjoy the gift. The gift now qualifies for the exclusion.

The "5 & 5" safe harbor matters too. When a withdrawal right lapses unused, the lapse is treated as a gift by the beneficiary.

The exception: the lapse falls within the greater of $5,000 or 5% of trust principal. This is a standard guardrail in any well-drafted irrevocable life insurance trust (ILIT).

5. Use the lifetime exemption deliberately

For estates likely to exceed $30,000,000 (2026), using lifetime exemption today locks growth outside the estate. For estates under the exemption, gifting low-basis assets often destroys value via the basis trade-off.

The sequence — exclusion first, qualified transfers, 529, trusts, lifetime exemption with cash — minimizes regret.

The Hidden Connection: Three Levers Many Advisors Coordinate Separately

One coordinated decision — gift cash, hold low-basis stock, superfund a 529 — touches three tax systems at once.

It changes your daughter's future capital-gains bill, your remaining lifetime exemption, and the size of your taxable estate at death. The dollars hide in the connections many advisors handle separately.

Here are three interactions very few articles ever measure:

Gift type ↔ recipient's future capital gains. A $1,000,000 cash gift carries no embedded tax. A $1,000,000 gift of low-basis stock carries the donor's basis under §1015. Same gift size; the cash version saves Sarah about $190,400.

Lifetime exemption use ↔ estate-tax shelter. Every dollar of taxable lifetime gifting reduces the unified credit at death. For families under $30,000,000 (2026), exemption use during life is a free move. For families over it, timing matters — growth on gifted assets escapes the estate.

Crummey trust funding ↔ estate inclusion if powers are retained. A grantor who funds an ILIT and keeps incidents of ownership pulls the death benefit back into the gross estate. The fix: fund through Crummey gifts without retained powers.

In the Covenant Wealth Advisors Strategy version of their story, the Hartmans run the same conversation differently. They give Sarah $76,000 of cash ($19,000 × 2 spouses × 2 years split December-January, zero filing).

They superfund a $190,000 couple 529 for their grandson. They pay $50,000 of tuition directly to the school. They hold their Apple stock to death, where Sarah's basis steps up under §1014 and any gain disappears.

Same family help. About $190,400 of capital-gains tax avoided. Lifetime exemption barely touched.

The real gift tax planning question is not what rate you would pay. It is which lever to pull, in which order, with which assets. The goal: no rate ever applies, and no basis is ever wasted.

What About Virginia State Gift Tax?

Virginia has no state gift tax — and never has. Virginia's state estate tax was repealed effective July 1, 2007 (Virginia Tax).

For Virginia residents, federal gift tax is the only transfer-tax constraint on lifetime giving. Virginia still charges a small probate tax on probate estates (Virginia Tax) — a filing-related charge, not a transfer tax.

Connecticut is currently the only state with its own state gift tax. If you or a recipient lives in or owns assets in Connecticut, more planning is required.

State rules change — verify current rules before relying on any state-level position. For our HNW clients across 22+ states, the federal rules in this article are the main framework.

Self-Assessment: Five Things to Check Before April 15

Here is what you can check right now, before the next Form 709 deadline.

Open last year's brokerage statements. Did you make any single gift over $19,000 to one person? If yes, Form 709 may be required even if no tax is owed. Find the gift, the date, and the basis.

Pull your most recent estate planning binder. Does your total estate exceed $30,000,000 (2026)? If yes, lifetime exemption planning is a live topic. If no, the basis trade-off matters more than exemption optimization.

List the 529 plans you funded last year. If a single contribution exceeded $19,000, was the 5-year election made on Form 709? If missed, the contribution may have eaten a lifetime exemption you didn't intend to use.

Identify any tuition or medical bills you paid for family members. Were the checks written directly to the school or provider? If they went to the family member first, the §2503(e) exclusion does not apply.

Check low-basis stock positions with basis under 50% of FMV. Are any earmarked for lifetime gifts? If yes, model the §1014 step-up alternative before you transfer.

Talk with a qualified advisor, CPA, or estate attorney before making changes.

Not Sure If You're Making the Right Retirement Decisions?

Schedule a free Strategy Session to discuss your situation and get honest answers.

What's keeping you up at night about retirement

How we approach tax planning, income, and investments differently

Whether we're the right fit—or if you're better off on your own

No pressure. No obligation. Just an honest conversation.

Frequently Asked Questions

Do I pay tax on a $20,000 gift?

If you give a $20,000 gift in 2026, you do not pay gift tax — but you must file Form 709 because the gift exceeds the $19,000 (2026) annual exclusion by $1,000.

The excess uses a small slice of your $15,000,000 (2026) lifetime exemption. If you receive a $20,000 gift, you owe nothing and report nothing (IRS).

Are gifts to children tax deductible?

No. Gifts to children — or to any individual — are not income-tax deductible. Only gifts to qualifying §501(c)(3) charities receive an income-tax charitable deduction.

Family gifts may use your $19,000 (2026) annual exclusion or $15,000,000 (2026) lifetime exemption, but neither produces a current-year income-tax deduction.

What happens if I miss the Form 709 deadline?

Form 709 is due April 15 of the year after the gift. The late-filing penalty is 5% per month of unpaid tax (capped at 25%) plus 0.5% per month for late payment.

Many missed filings owe no tax, so the dollar penalty is often zero. The bigger cost: the IRC §6501 3-year statute of limitations never starts running on an unfiled gift.

Can spouses combine the exclusion?

Yes. Married couples can elect gift-splitting under IRC §2513 on Form 709, treating all third-party gifts during the year as half from each spouse. The effect doubles the per-recipient annual exclusion to $38,000 (2026), made via a separate Notice of Consent.

Do I need to report a gift I received?

No. Federal law treats gifts received from a U.S. donor as non-taxable to the recipient (IRS). You owe nothing and report nothing on your federal income tax return. Gifts from foreign persons over $100,000 require info reporting on Form 3520 — info only, no tax owed.

What is the lifetime gift tax exemption for 2026?

The 2026 lifetime gift and estate tax exemption is $15,000,000 per individual / $30,000,000 per married couple, made permanent by the One Big Beautiful Bill Act (PL 119-21).

The exemption is unified across gift and estate tax — every dollar used during life reduces dollars available at death.

Ready to get the help you need to retire with peace of mind?

Contact us today for a Free Strategy Session.

About the author:

Chief Investment Officer

Andrew is the Chief Investment Officer for Covenant Wealth Advisors and a CERTIFIED FINANCIAL PLANNER™ practitioner. He has over 11 years of experience in the financial services industry in the areas of wealth management and financial planning for retirement.

Disclosures: Covenant Wealth Advisors is a registered investment advisor with offices in Richmond, Reston, and Williamsburg, VA. Registration of an investment advisor does not imply a certain level of skill or training. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. The views and opinions expressed in this content are as of the date of the posting, are subject to change based on market and other conditions. This content contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. This article was written and edited by a CERTIFIED FINANCIAL PLANNER™ professional with the assistance of AI. No advice may be rendered by Covenant Wealth Advisors unless a client service agreement is in place. Hypothetical examples are fictitious and are only used to illustrate a specific point of view. Diversification does not guarantee against risk of loss. While this guide attempts to be as comprehensive as possible, no article can cover all aspects of retirement planning. Be sure to consult an advisor for comprehensive advice.